Global / English

EVA Management

We use Economic Value Added (EVA®) as principal management metric. Continuously increasing EVA leads to greater corporate value, and corresponds not only to long-term benefit for shareholders but also for all of our stakeholders. The concept of “maximum with minimum” that we present in the K27 in fact represents the approach of EVA management. EVA could also be described as a metric that calculates how much true economic benefit is produced from invested capital. Management is always aware of invested capital since priority is given to obtaining profit in amounts exceeding the expected profit from the capital. The approach of “maximum with minimum” encompasses increasing Net Operating Profit After Tax (NOPAT) without increasing invested capital, through higher sales and reducing costs, and lowering cost of capital by, for example, improving our capital structure. This produces higher EVA and leads to enhancing corporate value. Although we have managed our businesses individually using numerical methods, we have not set target EVA values for each business, and instead use the EVA metric as a company-wide target. Our business divisions employ matrix management, where various functions including R&D, production and sales are encouraged to dynamically interact, while we manage capital efficiency as a single entity, because we believe this encourages proactive investments by business divisions and allows for flexible capital allocation according to the business circumstances. In K27, we will continue to use EVA a principal management metric while also implementing financial measures in anticipation of where the times are headed and continuing to innovate.

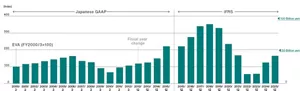

Improvement and Trends in EVA

We strive to increase corporate value by measuring improvement of EVA from the following four perspectives.

October 1998: Consulting by Stern Stewart & Co.* (first client in Japan)

April 1999: Started application of EVA

-

* Stern Stewart & Co.: Developed EVA in theory and applied it to corporate EVA management. Registered EVA as a trademark.

EVA (Economic Value Added) and ROIC (Return On Invested Capital)

1. Target Management Metrics

The Group uses EVA and ROIC as primary management metrics. The Group adopted EVA as a management metric in 1999 and has been promoting “EVA management” since its adoption. ROIC was introduced as a key management metric in August 2023 as part of our mid-term plan “K27.” The purpose of both indicators is to focus management on efficiently utilizing capital to generate profits from the perspective of shareholders and other capital providers. We believe that continuously increasing EVA leads to an increase in corporate value, which is in the long-term interests of all stakeholders. In our business, we use EVA for investment evaluations, annual performance management, and compensation systems with the aim of growing our business. Furthermore, we aim to deepen EVA management by strengthening business portfolio management through ROIC. ROIC raises awareness of capital costs in each business and enables management to better consider each business’s financial and operational characteristics and competitive environment. By emphasizing capital efficiency along with profits for each business, we aim to improve EVA through focused investment in growth businesses and thoughtful portfolio improvements.

2. Definitions and Calculation Methods of Metrics

The definitions and calculation methods of EVA and ROIC are as follows:

| Definition | NOPAT | Invested Capital | |

|---|---|---|---|

| EVA | The absolute amount of value creation exceeding capital costs (expressed in monetary value) | Net income + After-tax interest expense + Other one-time expenses (e.g., structural reform costs) |

Total equity + borrowings+ Bonds + Part of other financial liabilities*1 + Previously amortized goodwill and others*2 |

| EVA = Adjusted NOPAT - (Adjusted Invested Capital*3 ×WACC*4 ) | |||

| ROIC | The productivity of total investment (expressed as %) | Net income + After-tax interest expense |

Total equity + borrowings + Bonds + Part of other financial liabilities*1 |

| ROIC = NOPAT / Invested Capital*3 | |||

EVA and ROIC differ in the definitions of invested capital and NOPAT (Net Operating Profit After Taxes) used in the calculation process. EVA may capitalize and add one-time expenses such as restructuring costs to NOPAT to promote sustainable corporate value growth. Additionally, invested capital may include amortized goodwill and one-time expenses added to NOPAT.

-

* 1 Excluding lease liabilities.

-

* 2 Under previous Japanese GAAP, goodwill (and other items) that had already been amortized continued to be reflected in invested capital for our EVA calculation. This approach ensures that even investments that have been previously written off in our accounting records are still considered part of invested capital. By establishing a “high hurdle,” we rigorously assess whether our company is genuinely generating value that surpasses this threshold.

-

* 3 Average value at the beginning and end of the relevant fiscal year.

-

* 4 Calculated at the current rate of 5%.

3. Setting and Utilization of WACC in EVA

The capital cost rate used in EVA calculation is WACC (Weighted Average Cost of Capital), which is set based on the following considerations since EVA was introduced in 1999:

- Annual verification of the calculation and key inputs with external experts’ advice and independent data based on CAPM (Capital Asset Pricing Model)

- Stability considerations for medium- to long-term investment decisions

- Currently judged to be a reasonable level of 5% for Kao Group, with consistency confirmed with external data

- Home

- Investor Relations

- Management Information

- EVA Management

- Home

- Investor Relations

- Management Information

- EVA Management